The world’s rich are increasingly investing in expensive stuff, and “freeports” such as Luxembourg’s are becoming their repositories of choice. Their attractions are similar to those offered by offshore financial centres: security and confidentiality, not much scrutiny, the ability for owners to hide behind nominees, and an array of tax advantages. This special treatment is possible because goods in freeports are technically in transit, even if in reality the ports are used more and more as permanent homes for accumulated wealth. If anyone knows how to game the rules, it is the super-rich and their advisers.

Because of the confidentiality, the value of goods stashed in freeports is unknowable. It is thought to be in the hundreds of billions of dollars, and rising. Though much of what lies within is perfectly legitimate, the protection offered from prying eyes ensures that they appeal to kleptocrats and tax-dodgers as well as plutocrats. Freeports have been among the beneficiaries as undeclared money has fled offshore bank accounts as a result of tax-evasion crackdowns in America and Europe.

Several factors have fuelled this buying binge. One is growing distrust of financial assets. Collectibles have outperformed stocks over the past decade, with some, like rare coins, doing a lot better, according to The Economist’s valuables index. Another factor is the steady growth of the world’s ultra-wealthy population. According to Wealth-X, a provider of data on the very rich, and UBS, a financial-services firm, a record 199,235 individuals have assets of $30m or more, a 6% increase over 2012.

The goods they stash in the freeports range from paintings, fine wine and precious metals to tapestries and even classic cars. (Data storage is offered, too.) Clients include museums, galleries and art investment funds as well as private collectors. Storage fees vary, but are typically around $1,000 a year for a medium-sized painting and $5,000-12,000 to fill a small room.

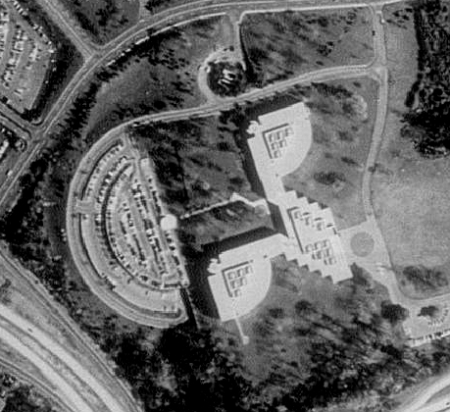

These giant treasure chests were pioneered by the Swiss, who have half a dozen freeports, among them sites in Chiasso, Geneva and Zurich. Geneva’s, which was a grain store in the 19th century, houses luxury goods in two sites with floor space equivalent to 22 football pitches. Luxembourg is not alone in trying to replicate this success. A freeport that opened at Changi airport in Singapore in 2010 is already close to full. Monaco has one, too. A planned “freeport of culture” in Beijing would be the world’s largest art-storage facility.

The early freeports were drab warehouses. But as the contents have grown glitzier, so have the premises themselves. A giant twisting metal sculpture, “Cage sans Frontières”, spans the lobby in Singapore, which looks more like the interior of a modernist museum or hotel than a storehouse. Luxembourg’s will be equally fancy, displaying concrete sculptures by Vhils, a Portuguese artist. Like Singapore and the Swiss it will offer state-of-the-art conservation, including temperature and humidity control, and an array of on-site services, including renovation and valuation.

The idea is to turn freeports into “places the end-customer wants to be seen in, the best alternative to owning your own museum,” says David Arendt, managing director of the Luxembourg freeport. The newest facilities are dotted with private showrooms, where art can be shown to potential buyers….Iron-clad security goes along with style. The Luxembourg compound will sport more than 300 cameras. Access to strong-rooms will be by biometric reading. Singapore has vibration-detection technology and seven-tonne doors on some vaults. “You expect Tom Cruise to abseil from the ceiling at any moment,” says Mark Smallwood of Deutsche Bank, which leases space for clients to store up to 200 tonnes of gold at the Singapore freeport.

Gold storage is part of Singapore’s strategy to become the Switzerland of the East. The city-state’s moneymen want to take its share of global gold storage and trading to 10-15% within a decade, from 2% in 2012. To spur this growth, it has removed a 7% sales tax on precious metals. (The Economist understands that the Luxembourg freeport’s gold-storage ambitions will get a fillip from the Grand Duchy’s central bank, which plans to move its reserves—now sitting in the Bank of England—to the facility once it opens. The bank declined to comment.)

Switzerland remains the world’s leading gold repository. Its imports of the yellow metal have exceeded exports by some 13,000 tonnes—worth $650 billion at today’s price—since the late 1960s, says the customs agency. The gap has widened sharply since the mid-2000s. But trade statistics do not tell the whole story, since they fail to capture the quantities of gold that go straight from runways to the freeports.

Wealth piled up in freeports is a headache for insurers. The main building in Geneva holds art worth perhaps $100 billion. The Nahmad art-dealing dynasty alone is said to have dozens of Picassos there. More art is stored in Geneva than insurers are comfortable covering, says Robert Read of Hiscox, an art insurer. Coverage for new items is hard to come by at any price….In a bid to soothe worries about concentrated storage, the private firm that operates Geneva’s freeport (which leases it from the majority owner, the local canton) is building a new warehouse a short distance from its existing structures. Most of the art is now stored in vaults under the main building. These were built in the 1970s as a way for banks to avoid a planned tax on gold held in their own vaults. The levy was repealed, the banks took back their gold, and paintings and sculptures soon began to fill the void. Luxembourg’s freeport, which is scheduled to open next summer, recently conducted a roadshow for insurers that highlighted the facility’s state-of-the-art safety features, including fire-fighting systems that suck oxygen from the air while releasing inert gas instead of water, so as not to damage art.

Insurance is cheaper for those willing to park assets in remote places. Switzerland is dotted with disused military bunkers, blasted into the Alpine rock during the second world war and cold war. The government has been selling these, and some have been bought by firms hoping to convert them into high-altitude treasure chests. One is Swiss Data Safe, which sells storage for valuables and digital archives at several undisclosed sites deep in the Gotthard granite. It claims to offer protection from “the forces of nature, civil unrest, disasters and terrorist attack”. Such places have a low risk of fire or being hit by a plane. But they cannot offer the tax advantages that freeports can.

Freeports are something of a fiscal no-man’s-land. The “free” refers to the suspension of customs duties and taxes…. this is all legal—though some countries have had to alter their statute books to accommodate the concept. Luxembourg amended its laws in 2011 to codify its freeport’s tax perks. That, plus the offer of land by the airport, helped persuade the project’s backers to put it there rather than in London or Amsterdam….Luxembourg’s government views the freeport as a useful adjunct to its burgeoning financial centre, which has been built on tax-friendliness. Deloitte, which helps firms and rich individuals minimise taxes, brokered the deal. Mr Arendt believes the freeport could help Luxembourg compete with London and New York in art finance, which includes structuring loans with paintings as collateral… As Swiss banks come under pressure to shop tax-dodgers, for instance, some are said to have been recommending clients to move money from bank accounts to vaults, in the form of either cash or bought objects, since these are not covered by information-exchange pacts with other countries. A sign that this practice may be on the increase is the voracious demand for SFr1,000 ($1,100) notes—the largest denomination—which now account for 60% of the value of Swiss-issued paper cash in circulation. Andreas Hensch of Swiss Data Safe says demand for its mountain vaults has been accelerating over the past year. The firm is not required to investigate the provenance of stuff stored there.

Western countries have started to clamp down on those who try to use such repositories to keep undeclared assets in the shadows. America has led the way. Under a bilateral accord, Swiss banks will have to deliver information on the transfer of funds from accounts, including cash withdrawals. Tax authorities are growing more interested in the contents of vaults. Americans with untaxed offshore wealth who sign on to an IRS voluntary-disclosure programme are required to list foreign holdings of art, says Bruce Zagaris of Berliner, Corcoran & Rowe, a law firm.

Tax-evaders are one thing, drug traffickers and kleptocrats another. In many ways the art market is custom-made for money laundering: it is unregulated, opaque (buyers and sellers are often listed as “private collection”) and many transactions are settled in cash or in kind. Investigators say it has become more widely used as a vehicle for ill-gotten gains since the 1980s, when it proved a hit with Latin American drug cartels. It is “one of the last wild-West businesses”, sighs an insurer. This makes freeports a “very interesting” part of the dirty-money landscape, though also “a black hole”, says the head of one European country’s financial-intelligence agency. In a report in 2010 the Financial Action Task Force, which sets global anti-money-laundering standards, fretted that free-trade zones (of which freeports are a subset) were “a unique money-laundering and terrorist-financing threat” because they were “areas where certain administrative and oversight procedures are reduced or eliminated”.

Numerous investigations into tainted treasures have led to freeports. In the 1990s hundreds of objects plundered from tombs in Italy and elsewhere were tracked down to Geneva’s warehouse (along with papers showing that some had been laundered by being sold at auction to straw buyers, then handed straight back with the legitimate purchase documents). In 2003 a cache of stolen Egyptian treasures, including two mummies, was discovered in Geneva; in 2010 a Roman sarcophagus turned up there, perhaps pinched from Turkey.

Under pressure to respond, the Swiss have tightened up their laws on money-laundering and the transfer of cultural property. A law that took effect in 2009 brought Switzerland’s freeports into its customs territory for the first time. They must now keep a register of handling agents and end-customers using their space. Handlers must keep inventories, which customs can request to see.

In practice, however, clients can still be sure of a high degree of secrecy. Swiss customs agents still care more about drugs, arms or explosives than about the provenance of a Pollock. They do not have to share information with foreign authorities. Much of it is of limited value anyway, since items can be registered in the name of any person “entitled” to dispose of them—not necessarily the real owner.

Even greater secrecy is on offer in Singapore. Goods coming in to the freeport must be declared to customs, but only in a vague way: there is no requirement to disclose owners, their stand-ins or the value or precise nature of the goods (“wine” or “antiques” is enough). “We offer more confidentiality than Geneva,” Mr Vandeborre declared when the facility opened. However, it is not quite true to say that Singapore and other new sites are in arm’s-length competition with the more established facilities. In fact, they share the same tight-knit group of mostly Swiss owners, managers, advisers and contractors. Yves Bouvier, the largest private shareholder in the Geneva freeport, is also the main owner and promoter of the Luxembourg freeport, a key shareholder in Singapore and a consultant to Beijing. His Geneva-based art-handling firm, Natural Le Coultre, is closely involved in running or setting up all these operations. Singapore’s architects and engineers were Swiss, as are its security consultants.

This has fuelled speculation that Swiss interests have deliberately developed a strategy to globalise the high-end freeport concept as a way to continue to benefit, even as the crackdown on undeclared money in Zurich and Geneva drives some of it to other countries. Franco Momente of Natural Le Coultre rejects this interpretation. “It’s nothing more than supply and demand,” he says. “Today many countries see the advantages of freeports for the local economy and to have a place in the global art market. They’re looking for solutions with experienced operators, and [the Swiss] have long experience.”

Barring dramatic regulatory intervention or moves to end their tax benefits, freeports are likely to grow, driven primarily by clients in emerging markets. At current growth rates the collective wealth of Asia’s rich will overtake Europe’s by 2017, reckon UBS and Wealth-X (see chart 2). As this population grows, so too could wealth taxes in the region, which are now low or non-existent. That could drive yet more Indians, Chinese and Indonesians towards the discreet duty-free depots which—if they aren’t already there—may soon be coming to an airport near you.

Freeports: Über-warehouses for the ultra-rich, Economist, Nov. 23, 2013, at 27

Nigeria and Switzerland signed a memorandum of understanding on March 26, 2018 to pave the way for the return of illegally acquired assets…Switzerland said in December 2017 that it would return to Nigeria around $321 million in assets seized from the family of former military ruler Sani Abacha via a deal signed with the World Bank…[T]he memorandum of understanding was ratified between Nigeria, Switzerland and the International Development Association, (IDA), the World Bank’s fund for the world’s poorest countries.

Nigeria and Switzerland signed a memorandum of understanding on March 26, 2018 to pave the way for the return of illegally acquired assets…Switzerland said in December 2017 that it would return to Nigeria around $321 million in assets seized from the family of former military ruler Sani Abacha via a deal signed with the World Bank…[T]he memorandum of understanding was ratified between Nigeria, Switzerland and the International Development Association, (IDA), the World Bank’s fund for the world’s poorest countries.

A SpaceX Falcon rocket lifted off from the Kennedy Space Center in Florida on May , 2017 to boost a classified spy satellite into orbit for the U.S. military, then turned around and touched down at a nearby landing pad.

A SpaceX Falcon rocket lifted off from the Kennedy Space Center in Florida on May , 2017 to boost a classified spy satellite into orbit for the U.S. military, then turned around and touched down at a nearby landing pad.

A real-estate magnate is financing Google’s and Facebook Inc.’s new trans-Pacific internet cable, the first such project that will be majority-owned by a single Chinese company. Wei Junkang, 56, is the main financier of the cable between Los Angeles and Hong Kong, a reflection of growing interest from China’s investors in high-tech industries. It will be the world’s highest-capacity internet link between Asia and the U.S.

A real-estate magnate is financing Google’s and Facebook Inc.’s new trans-Pacific internet cable, the first such project that will be majority-owned by a single Chinese company. Wei Junkang, 56, is the main financier of the cable between Los Angeles and Hong Kong, a reflection of growing interest from China’s investors in high-tech industries. It will be the world’s highest-capacity internet link between Asia and the U.S.

Authorities in Switzerland are in talks to arrange the return to Nigeria of $300 million confiscated from the family of its former military ruler, Sani Abacha, Nigeria’s foreign minister said. The corruption watchdog Transparency International has accused Abacha of stealing up to $5 billion of public money during his five years running the oil-rich nation, from 1993 until his death in 1998. Foreign Minister Geoffrey Onyeama said $700 million had already been repatriated from Switzerland, adding that he met Swiss representatives last week for further talks. “They have also now recovered, in the same context, another $300 million of which there is ongoing discussion to have that repatriated as well,” he told journalists on Monday.

Authorities in Switzerland are in talks to arrange the return to Nigeria of $300 million confiscated from the family of its former military ruler, Sani Abacha, Nigeria’s foreign minister said. The corruption watchdog Transparency International has accused Abacha of stealing up to $5 billion of public money during his five years running the oil-rich nation, from 1993 until his death in 1998. Foreign Minister Geoffrey Onyeama said $700 million had already been repatriated from Switzerland, adding that he met Swiss representatives last week for further talks. “They have also now recovered, in the same context, another $300 million of which there is ongoing discussion to have that repatriated as well,” he told journalists on Monday.